CBDCs vs Stablecoins: What Are the Key Differences?

CBDCs vs Stablecoins: What Are the Key Differences?

The trend of countries implementing CBDCs raises questions about decentralization, particularly as central banks hold significant control over these digital currencies.

by Thomas Thang, senior investment associate

China recently included its retail CBDC, e-CNY, into its December 2022 M0 money supply data.

M0, also called "base money", is the most liquid measure of money supply, including physical currency (i.e. banknotes and coins) in circulation and commercial banks' reserve balances held at central banks.

In this article, we address the misconceptions surrounding Central Bank Digital Currencies (CBDCs) and stablecoins, as well as the implications of decentralization.

Definitions:

CBDCs are digital versions of a country's fiat currency issued by a country’s central bank.

It is widely believed CBDCs must be built on blockchain or distributed ledger technology (DLT). However, this notion is mistaken as CBDCs have already been implemented within centralized systems.

Wholesale CBDC

Central bank money has been available in digital form for wholesale transactions between banks for decades. These ‘wholesale CBDCs’ have been a core component of modern financial systems, used for digital interbank transactions within real-time gross settlement systems to harmonize post-trade services and simplify cross-border collateral settlements.

Photo by Chris Liverani on Unsplash

Retail CBDC

A retail CBDC is a digital payment instrument and a direct liability of the central bank which is usable by the general public for everyday transactions. It is effectively ‘digital cash’ like China’s e-CNY or India’s e-rupee. This is not to be confused with electronic or mobile money, which is the liability of commercial banks and other financial institutions. This is why you need a bank account to transact electronically. CBDCs may be universally accessible and can operate without a bank account, which can remove the need for a trusted financial intermediary.

Decentralized CDBCs

Central banks have the option to choose the level of decentralization they wish to implement in their CBDCs. This can range from a centralized private ledger to a fully decentralized public blockchain, with various options in between, but they all come with trade-offs. Greater transparency and verifiability can be achieved through increased decentralization, but this can also result in decreased privacy and increased costs and latency. In any case, CBDCs are ultimately still controlled and influenced by the central bank and its monetary policies. Thus, the term "decentralized CBDC" may be considered an oxymoron.

Stablecoins

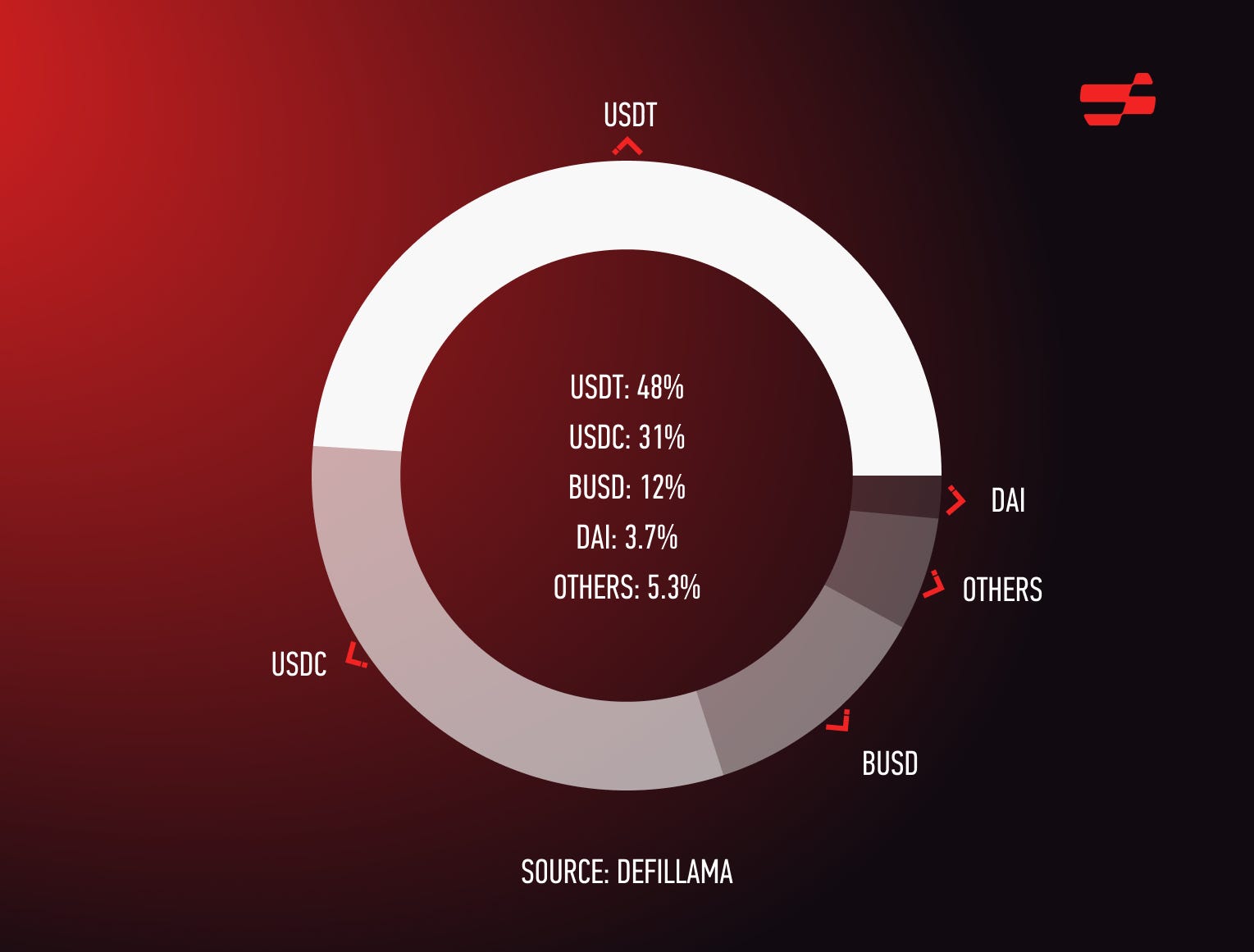

Stablecoins are digital currencies whose value is pegged to another reference asset, such as a fiat currency or gold. Stablecoins are issued by a third-party institution or protocol that may guarantee or maintain the stability of the peg to the reference asset. Stablecoins like USDC or USDT are maintained by centralized entities, while DAI is issued by a decentralized protocol and maintained via various mechanisms and economic incentives.

Conclusion

Central banks still lie at the intersection of both CDBCs and stablecoins. CBDCs, such as China's e-CNY and India’s e-rupee, are directly issued and controlled by the central bank, while stablecoins are typically pegged to a fiat currency, also under the purview of the issuing central bank.

The concept of a truly decentralized stablecoin, operating on a fully decentralized public blockchain, is yet to be fully realized and the potential for widespread adoption remains uncertain.